In today’s financial landscape, finding ways to save on taxes is a top priority for many individuals. One often-overlooked tool for tax savings is the Health Savings Account (HSA). In this article, we will delve into the ins and outs of HSAs and explore how you can leverage them to maximize your tax benefits while securing your healthcare needs. So, let’s embark on a journey to unravel the potential tax-saving benefits of your HSA.

Understanding the Basics of an HSA

Before we dive into the tax-saving strategies, it’s essential to grasp the fundamental concepts behind an HSA.

What is an HSA?

If you’re enrolled in a High Deductible Health Plan (HDHP), you may be eligible for a Health Savings Account (HSA). This type of savings account offers a range of healthcare and tax benefits. You can use your HSA funds to cover eligible medical expenses like doctor’s visits, prescriptions, and medical procedures. However, it’s important to remember that using your HSA card for non-medical expenses can result in penalties and taxes. If i accidentally used my hsa card for groceries, be sure to inform your HSA provider and repay the amount promptly to avoid any negative consequences.

Contributions and Limits

To leverage your HSA effectively, you need to understand the contribution limits. These limits can change annually, so it’s crucial to stay updated on the latest figures.

Individual Limits

- 2023 HSA contribution limit for individuals: $3,650

- Additional catch-up contribution (age 55+): $1,000

Family Limits

- 2023 HSA contribution limit for families: $7,300

- Additional catch-up contribution (age 55+): $1,000

Tax Advantages

One of the primary reasons individuals opt for an HSA is the tax benefits it offers. Contributions are tax-deductible, and withdrawals for qualified medical expenses are tax-free.

Leveraging Your HSA for Tax Savings

Now that we have a solid grasp of the HSA basics, let’s explore some strategies to maximize your tax savings.

1. Maximize Your Contributions

Contributing the maximum allowed to your HSA is the first step to optimizing your tax savings. By doing so, you reduce your taxable income, leading to lower tax liability.

2. Invest Your HSA Funds

Many people are unaware that you can invest your HSA funds once they reach a certain balance. Investing can help your HSA grow over time, offering potential tax-free gains.

3. Use HSA Funds Strategically

Consider using your HSA funds strategically. You can pay for qualified medical expenses out of pocket and let your HSA funds grow tax-free. This way, you can save your HSA balance for future healthcare needs or retirement.

4. Keep Records of Medical Expenses

To claim tax-free withdrawals, you must maintain records of your medical expenses. Be diligent about saving receipts and documenting eligible expenses.

5. Plan for Retirement

HSAs can serve as a valuable retirement savings tool. After age 65, you can withdraw funds for non-medical expenses without penalties. However, regular income tax applies, similar to a traditional IRA.

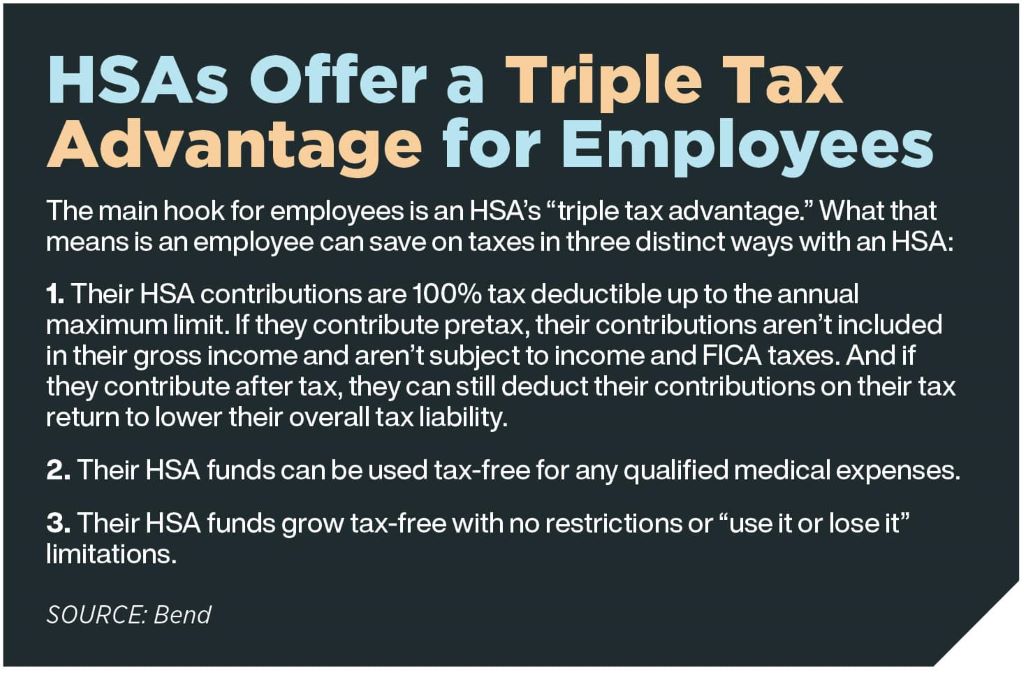

6. Consider the Triple Tax Benefit

HSAs offer a unique triple tax benefit: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses. Few financial instruments provide such a comprehensive tax advantage.

In conclusion, leveraging your Health Savings Account (HSA) for tax savings is a smart financial move. By understanding the basics of HSAs and implementing the strategies mentioned above, you can take full advantage of the tax benefits they offer, which can be especially beneficial for various types of business ideas. Maximize contributions, invest wisely, and plan for the long term to secure your financial future while minimizing your tax burden.

FAQs (Frequently Asked Questions)

- Can I open an HSA if I don’t have a High Deductible Health Plan (HDHP)?

No, you must be enrolled in an HDHP to qualify for an HSA. It’s a requirement set by the IRS.

- Are there penalties for using HSA funds for non-medical expenses before age 65?

Yes, if you withdraw funds for non-medical expenses before age 65, you may face a 20% penalty in addition to regular income tax.

- Are HSA contributions tax-deductible even if I don’t itemize deductions?

Yes, HSA contributions are an above-the-line deduction, which means you can deduct them from your taxable income even if you don’t itemize deductions.

- Can I use my HSA to pay for my family’s medical expenses?

Yes, you can use your HSA funds to pay for qualified medical expenses for yourself, your spouse, and your dependents.

- How do I invest my HSA funds, and what are the investment options?

You can typically invest your HSA funds in various investment options, such as mutual funds, stocks, and bonds, depending on your HSA provider. Check with your HSA administrator for specific investment choices and instructions.

Now that you’re armed with knowledge on how to leverage your HSA for tax savings, take the necessary steps to optimize your financial well-being. Remember, financial planning and tax strategies can evolve, so stay informed to make the most of your HSA and other financial tools.